Fintech Newsletter for 4/17/21

Below are news related to fintech industry this week.

General News

Bank Earnings

Last week big American banks reported their quarterly earnings. Some of the common sentiments shared by the business leaders in the banking world on earnings call were as follows,

(a) Bullish on economic recovery: Banks expected a faster recovery than previously expected recovery that was stretching into 2022.

(b) Banks released "reserves" boosting their Net Incomes: High liquidity in markets due to lower interest rates has caused borrowers to return the money, which resulted in banks making changes in their books to release the "reserves".

What are reserves?

Some accounting background, In simple terms, reserves are money kept aside by the bank expecting that all borrowers will not return loans in full. Banks either "build," i.e., increases the "reserves" in anticipation of a high-risk environment, or "releases," i.e., decreases the "reserves" when the risk conditions are manageable.

Calculate Reserve Build (or Release) by subtracting net charge-offs from the Provision for credit losses recognized in that period.

Reserve = Provision of credit loses - Net Charge off.

"Provision for credit losses" is an expense account on the income statement. A bank based on historical trends of loan recovery will set this value.

A "Net charge-off" is the final "bad debt" that the bank must write off as losses.

Net charge-off = Gross charge-off - Partial recovered debt

For example, if a bank provided $100 in loan and expects $10 worth of losses on loans(based on historical precedence) and as the quarter continues, lets say $10 is, in fact, the losses (i.e., the borrower is unable to return ). However, if part of the losses, say $6, is recovered before the end of the quarter. Then $10 will be both "Provision for credit loss" and "gross-charge off" and $4 will be the net-charge off.

Net-Charge off =10-6=4 and Reserve=10-4=6

Now let say, if the economic condition has become good and the creditor(i.e., the borrower) for the current quarter can repay loans from previous quarters, then the bank will set the "Provision for credit loss" as -$10, and if "net-charge off" for the quarter is $4,then

Reserve =-10-4=-14 , (i.e reserve is released) Let's take a look at Bank of America Income statement for 1Q2021 (all amount in $millions)

Net interest income :10,308

Non interest income :12,624

Total Revenue :22,932

Non interest expense :15,515

Provision for credit loss: -1860

Net Income before taxes = 22,932-15,515- (-1860) = 9,277Now let's look at net charge -offs, for 1Q2021 BAC reported $823M in net char-offs.

So total reserve "release" = -1860-823= -2,683M => approx $2.7B Bank of America (NYSE:BAC) 1Q21 Earnings

BAC for the 1Q21 quarter reported revenue of $22.93B which was almost flat YoY with a Net Income of $8.1B, which was 50% higher YoY. BAC reported a $2.7B reserve release.

We do have some work to do in certain areas as we have for the last decade. I'd highlight those three areas with a couple of comments on each. Those areas are loan growth, net interest income and expense"-Brian Moynihan - Chairman, President, and Chief Executive Officer (BAC)

Wells Fargo (WFC) Earnings 1Q21 Earnings

WFC for the 1Q21 reported revenue of $18.06B which was almost flat YoY with a Net Income of $4.7 billion. WFC reported a $1.05B in reserve release.

Overall economic trends improved during the quarter, and while there are risks, the likelihood of improvement continues to increase, and you certainly see this in the markets. Equity markets are rising. Spreads have tightened, and liquidity is strong. Additional fiscal stimulus continued monetary support, and the acceleration of vaccine availability provides a path to a more complete reopening and further economic expansion. U.S. GDP growth is on track to surpass its pre-pandemic peak by the end of the summer and is expected to increase in 2021 by more than any year since 1984" Charlie Scharf, CEO (WFC)

Citigroup Inc (NYSE: C) Earnings

C for 1Q21 reported a Revenues of $19.3B and a Net Income of $7.9 billion.C reported a $3.85B in reserve release.

Citigroup announced new plans for Asia and EMEA, and Jane explained strategy on consumer banking targeting specific critical geographies and focusing on institutional clients for remaining centers in Asia and EMEA.

we announced our decision to focus our consumer banking franchise in Asia and EMEA solely on four wealth centers, namely Singapore, Hong Kong, UAE, and London…....... We will, therefore, pursue exits of our consumer businesses in the remaining 13 markets in Asia and EMEA...........Citi will continue to invest behind and serve our institutional clients in these 13 markets. We have a high-returning and leading institutional franchise in Asia, and it is an absolutely central part of our success going forward." Jane Fraser -CEO(C)

Other banks that reported earnings last week included Morgan Stanley (M.S.), reporting $4.1B Net Income on a $15.72B revenue. Goldman Sachs(G.S.) reporting $6.1B Net Income on a $17.7B revenue. Bank of New York Mellon(BNY) reported a $3.26B in revenue.

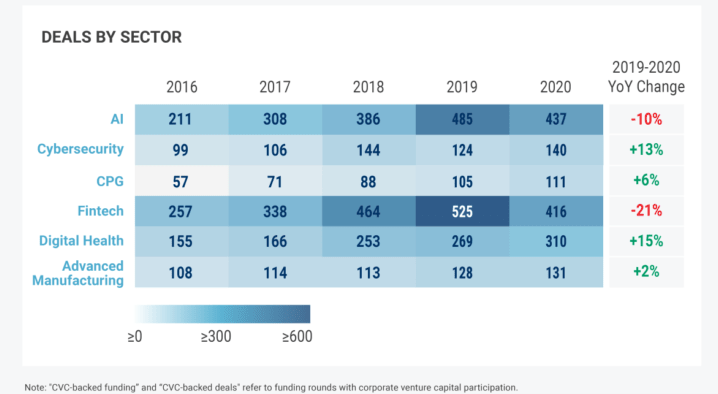

2020 Global CVC report by CBInsights.

CBInsights released a report available on their website . The report highlights the venture deals for last year. Even though the "Fintech" sector is in the second position in the below table, it had the maximum decline in the deal activity compared to previous years. Similarly "A.I." sector, even though it had the highest number of deals in 2020, was the sector with the second-highest decline during the pandemic. Interestingly digital health (with a 15% increase from prior year ) and cybersecurity (with a 13% increase from prior year) were the top two areas for venture deals during the pandemic.

Fintech New Venture and IPO

- Level, New York Based maker of financial products for employers, raised $27m in series A funding.

- Ramp,spend management startup,raised $115m in funding.

- Sunday, an Atlanta-based restaurant payment app, raised $24m in seed funding.

- Routable, San Francisco-based B2B payments company, raised $30m in Series B funding.

- IPO-Coinbase fetched $85b valuations in stock market debut.

- Wage, San Francisco-based payroll data sharing company, raised $5m in seed funding.

- Hatch, San Francisco, based neobank for SMBs raised $20m in new funding.

- ConsensSys, a New York-based Etherium startup studio, raised $65m in new funding.

- Clearcover, Chicago based car insurance startup, raised $20m in series D funding.

- Zebra, an Austin-based insurance comparison site, raised $150m in series D funding.

If you have any comments or have any topic requests for the blog, please leave your feedback here.