What is Card Present (CP) Transaction?

In this post, we will look at the Card Present (CP) transaction.

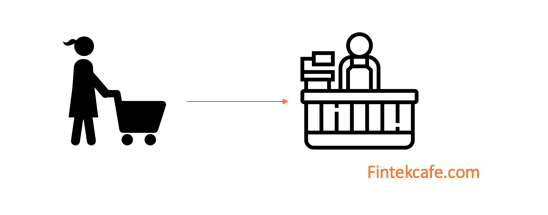

Say you have a credit card from your bank. You go to your favorite grocery store and finish shopping. At checkout, you insert your credit card into the Point of Sale (POS) terminal. That is a CP transaction.

In simple terms, a Card Present (CP) transaction happens whenever a merchant can read the electronic information from your card directly at the time of purchase.

You might wonder if using a digital wallet at a coffee shop counts as a Card Present (CP) transaction. The answer is yes.

Your card can be physical or digital. As long as the merchant can read the electronic card information directly from you, it is a Card Present (CP) transaction.

Here are some examples of CP transactions:

- An old-school credit card machine at checkout

- A modern POS (Point of Sale) terminal

- A contactless-enabled terminal (such as NFC)

- A merchant card reader connected to a smartphone

Important note: if the merchant takes your credit card and manually types in the card number, expiration date, and CVV (Card Verification Value), that purchase is not a CP transaction.

OK, this is great, but why do we need to make such a distinction?

Like everything in life and business, it comes down to risk management.

CP transactions usually happen in person. A fraudster is less likely to use a stolen card in person than to make a purchase over the phone or on a website.

Merchants also get more chargeback protection with CP transactions. (A chargeback is when a customer reports a fraudulent transaction on their credit card to their bank. We will cover chargebacks in more detail in another post.)

With CP transactions, merchants can provide detailed records and extra evidence, such as security camera footage. This helps reduce their responsibility to pay for chargebacks. In these cases, the issuer bank (the bank that gave the customer their credit card) will cover the fraud charges.

All transactions that are not CP are called Card Not Present (CNP).

So, how does CP transactions work?

Step 1: The customer finishes shopping in-store and goes to the cashier at checkout.

Step 2: The customer either inserts an EMVCo chip card or uses a digital wallet with NFC at the POS device.

Step 3: The merchant's POS device contacts the credit card processor to complete the transaction.

What are the common methods to protect against CP fraud?

As a consumer, here is what you can do:

(a) The moment you realize you have lost your credit card, call your bank right away. Ask them to block the current card and issue a new one.

(b) Check your credit card statements regularly. Sign up for any free alert services your bank offers. If you spot a fraudulent transaction, call your bank immediately to block the card.

Credit networks and banks also provide best practices for merchants. Here are some common ones:

(a) Use an EMV/EMVCo chip reader. This helps reduce liability for the merchant.

(b) Merchants can ask for additional ID verification from customers during checkout.

(c) Merchants should train their cashiers to notice and report unusual behavior. Examples include multiple small purchases on the same day or customers creating distractions at checkout.

(d) Regularly check POS devices for any signs of tampering, such as missing screws or loose wires.

Related Articles

Payment Orchestration: Why Merchants Route Across Multiple Processors

At scale, single-processor checkout is a point of failure and a margin leak. How payment orchestration routes across processors to lift authorization rates.

Pay by Bank: How Account-to-Account Payments Threaten Card Interchange

Account-to-account payments let merchants pull funds straight from a bank account and skip card interchange. How pay by bank works and why it threatens cards.

Real-Time Fraud Detection: How Payments Risk Moved to Milliseconds

Instant payments removed the float fraud teams relied on. A 2026 framework for sub-second scoring, the model stack, and build versus buy.